ARVINAS (ARVN)·Q4 2025 Earnings Summary

Arvinas Q4 2025: Revenue Drops 84% as Milestone Timing Shifts, but Vepdegestrant PDUFA Looms

February 24, 2026 · by Fintool AI Agent

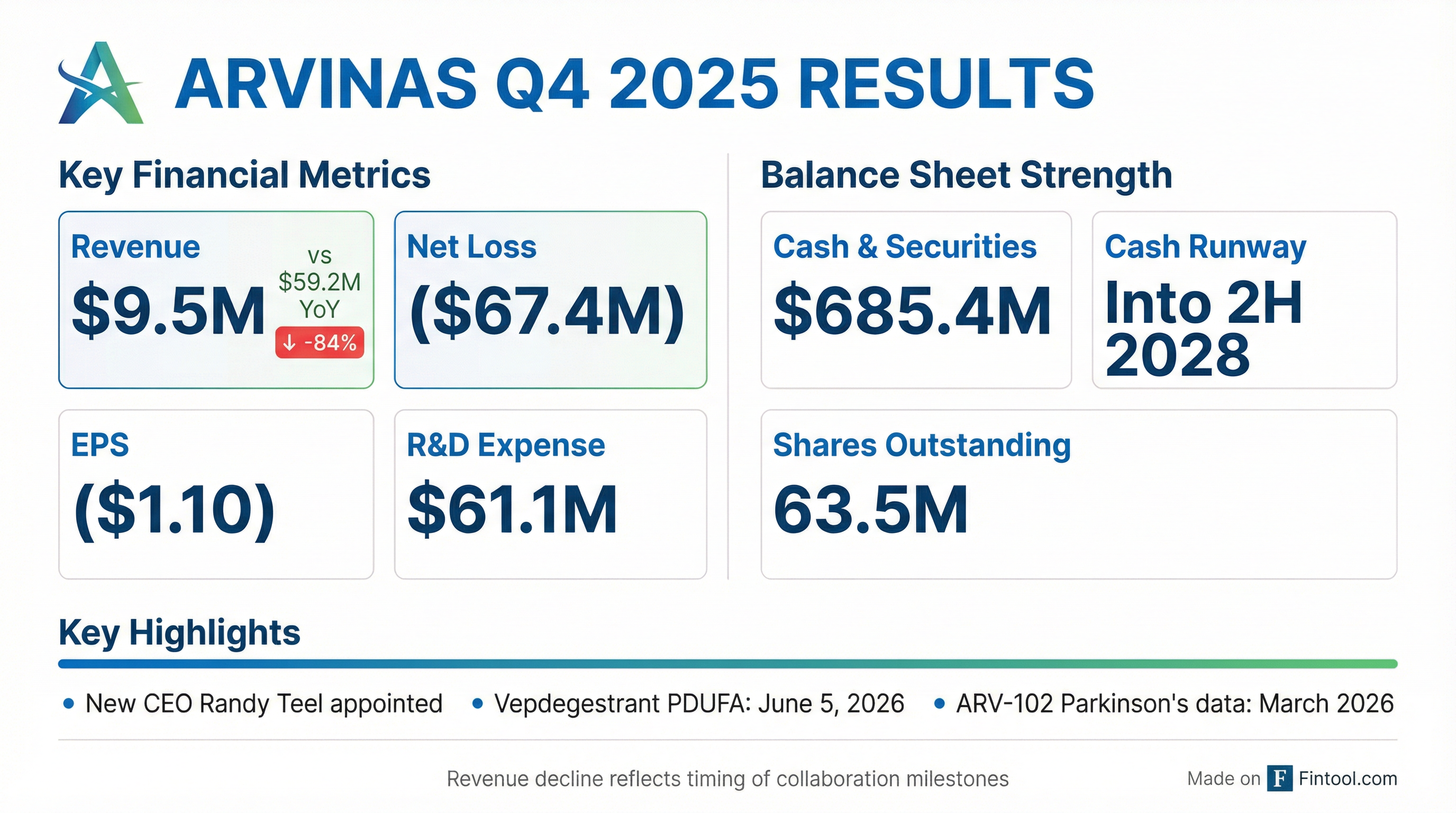

Arvinas (NASDAQ: ARVN) reported Q4 2025 results that reflected the lumpy nature of biotech collaboration revenue, with the quarter weighed down by the absence of prior-year milestone payments. Revenue fell 84% year-over-year to $9.5M while the net loss widened to -$67.4M (-$1.10 EPS) . The stock traded down approximately 4.5% in after-hours following the release.

The headline numbers mask what management described as "meaningful progress" across the pipeline . With four clinical trials ongoing (and a fifth, HPK1 degrader ARV-6723, expected to enter clinic later this year), a potential first-ever PROTAC FDA approval on the horizon (vepdegestrant PDUFA: June 5, 2026), and cash runway extending into 2H 2028, the setup for 2026 is catalyst-heavy . New CEO Randy Teel emphasized a "differentiation or nothing" strategy on the call, setting high bars for each program to advance .

What Did Management Say?

New CEO Randy Teel set the tone for the call with a focus on differentiation:

"We won't settle for as good as, and we hope patients don't have to choose between efficacy, safety, and tolerability. We're determined to only develop treatments that are differentiated and will be highly disciplined in moving programs forward."

On the company's strategic positioning:

"Very few phase I companies have such a strong pipeline and the capital to reach important milestones, and even fewer have a platform that's already announced positive phase III clinical trial results."

CMO Noah Berkowitz on ARV-102's competitive differentiation in LRRK2:

"We've shown already in healthy volunteers that we can achieve more than 50% LRRK2 degradation in the brain. That's been our target... something that can't be touched by inhibitors."

On ARV-393 BCL6 responses:

"If you're in the business of drug development and you have a new mechanism of action, and you see a drug that can achieve a complete metabolic response in patients that otherwise have a deadly disease, you remain very committed and enthusiastic about the future for that product."

Did Arvinas Beat Earnings?

No. Q4 2025 results came in below expectations on both revenue and earnings:

Context matters: The revenue decline was driven entirely by collaboration milestone timing, specifically the completion of the Novartis technology transfer for luxdegalutamide in 2024, which contributed $40.3M to Q4 2024 revenue that did not repeat . Operating expenses declined significantly as the company sharpened its pipeline focus.

How Did the Stock React?

ARVN closed at $12.30 on February 23, 2026, then dropped to $11.74 in after-hours trading following the release—a decline of approximately 4.5%.

Historical earnings reactions:

Current positioning:

- YTD 2026: +7.2%

- 52-Week Range: $5.90 - $18.93

- Market Cap: ~$903M

The muted reaction relative to prior quarters suggests investors are looking past near-term financials toward the June 5 vepdegestrant PDUFA date.

What Changed From Last Quarter?

Leadership Transition

Randy Teel, Ph.D. was appointed President, CEO, and Director, succeeding founder John Houston, Ph.D., who retired but remains on the Board and entered a consulting agreement . Briggs Morrison, M.D. was elected Board Chair.

Pipeline Advancement

Four clinical programs now in active trials, up from three last quarter, with a fifth (ARV-6723) expected to enter clinic by year-end:

- ARV-102 (LRRK2 for Parkinson's): Multiple dose Phase 1 data accepted for oral presentation at AD/PD Conference in March 2026

- ARV-806 (KRAS G12D): Completed dose escalation well ahead of plan; initial clinical data expected mid-2026

- ARV-393 (BCL6 for NHL): Complete metabolic responses observed in early cohorts; combination trial with glofitamab planned H1 2026

- ARV-027 (polyQ-AR for SBMA): Phase 1 recently initiated in healthy volunteers—new addition this quarter

- ARV-6723 (HPK1 for I-O): Preclinical data at AACR I-O Conference; first-in-human planned later in 2026

Strategic Shift on Vepdegestrant

Arvinas and Pfizer announced plans to identify a third-party partner for commercialization and potential further development of vepdegestrant, rather than co-commercialize themselves .

What Did Management Guide?

Cash Runway

$685.4M in cash, cash equivalents, and marketable securities as of December 31, 2025, providing runway into the second half of 2028 .

The cash decline reflects:

- Operating cash burn of ~$261M for full-year 2025

- Share repurchases of $91.9M (~10M shares at average price of $9.09) under the Stock Repurchase Program, now suspended with no further repurchases planned

No Explicit Financial Guidance

Arvinas does not provide quarterly revenue guidance given the milestone-driven nature of its revenue model.

What Are the Key Catalysts Ahead?

Near-Term (H1 2026)

Back Half 2026

Pipeline Deep Dive

Vepdegestrant (ER Degrader) — Pfizer Partnership

The most near-term value driver. Key facts:

- VERITAC-2 Phase 3: Demonstrated statistically significant PFS improvement vs. fulvestrant in ER+/HER2- ESR1-mutated advanced breast cancer

- PDUFA Date: June 5, 2026

- Fast Track Designation: Granted by FDA

- Partner Search: Discussions with potential partners have been "productive"; goal is to have agreement in place before the June 5 PDUFA date

- Roche Validation: Management noted recent Roche ER degrader data validates the hypothesis that ER therapy works where ER drives disease

If approved, vepdegestrant would be the first-ever FDA-approved PROTAC protein degrader, validating the entire platform technology.

ARV-102 (LRRK2 Degrader) — Neurology Lead

Targeting LRRK2 for Parkinson's disease and progressive supranuclear palsy (PSP):

- Mechanism: Oral, brain-penetrant PROTAC designed to degrade the entire LRRK2 protein complex, disrupting kinase, GTPase, and scaffolding functions linked to neuroinflammation and lysosomal dysfunction

- Clinical Data: Already demonstrated >50% LRRK2 degradation in CSF, dose-dependent CSF exposure, and reduction of downstream pathway biomarkers (GPNMB, CD68) in healthy volunteers

- March 2026: Phase 1 multiple dose data in PD patients at AD/PD Conference—will show pathway biomarker results

- H1 2026: Phase 1b initiation in PSP planned, targeting PSP-RS patients (~40% of PSP population)

- Late 2026: Potential registrational trial in PSP pending health authority feedback

ARV-806 (KRAS G12D Degrader) — Oncology Lead

Targeting the most common KRAS mutation in solid tumors:

- Differentiation: Preclinical data showed >25-fold greater potency vs. clinical-stage inhibitors; potent and selective elimination of both on and off forms of the protein

- Durable degradation: >90% degradation sustained for 7 days after a single dose, with efficacy across pancreatic, colorectal, and lung cancer models

- Phase 1 Progress: Dose escalation completed for once-weekly dosing well ahead of plan, reflecting strong clinical investigator interest

- Initial Data: First data disclosure expected by mid-2026; already submitted for presentation at a medical congress

- Competitive Bar: Management acknowledged need to exceed ~35% response rates seen with competing programs to demonstrate differentiation

ARV-393 (BCL6 Degrader)

Targeting B-cell lymphomas with potential to become chemo-free standard of care:

- Mechanism: BCL6 has rapid resynthesis rate making it difficult to target with inhibitors; ARV-393's iterative event-driven mechanism counters this with potent, sustained degradation

- Early Signal: Complete metabolic responses observed in early cohorts at doses below predicted effective exposure, in both B- and T-cell lymphomas

- Combination Potential: 91% tumor growth inhibition with ARV-393 + glofitamab sequentially vs. 36% for glofitamab alone; RNA sequencing showed enhanced CD20 expression and pro-inflammatory signaling

- Next Steps: Phase 1 combination trial with glofitamab in DLBCL planned for H1 2026; no dose modifications anticipated due to non-overlapping toxicity profiles

ARV-027 (polyQ AR Degrader) — Newly Initiated

Targeting spinal and bulbar muscular atrophy (SBMA/Kennedy's disease):

- Rationale: SBMA is an X-linked disease caused by polyglutamine-expanded AR accumulation in muscle; no approved disease-modifying therapies exist

- Preclinical Data: Oral ARV-027 induced robust polyQ AR degradation in muscle, resulting in improved grip strength, endurance, and extended survival in SBMA mouse model

- Phase 1 Status: Recently initiated in healthy volunteers; will include SBMA patients later with muscle biopsy endpoints

- Expertise: Third AR degrader from Arvinas platform; luxdegalutamide outlicensed to Novartis for up to $1B in 2024

ARV-6723 (HPK1 Degrader) — Upcoming IND

First immuno-oncology PROTAC targeting solid tumors:

- Target: HPK1 acts as central intracellular brake on immune system; degradation eliminates both kinase and scaffolding functions

- Preclinical Results: Meaningful and durable tumor growth control as single agent across multiple syngeneic models; outperformed HPK1 inhibitor and anti-PD-1 therapy in several settings

- Mechanism: Induces pro-inflammatory tumor microenvironment with increased activated T cells, NK cells, and monocytes; reduces immunosuppressive neutrophils

- Timeline: First-in-human studies planned for later in 2026 pending regulatory feedback

Pan-KRAS Program — Preclinical

Complementary program to ARV-806 targeting broader KRAS mutation landscape:

- Scope: Designed to degrade KRAS across all alterations including wild-type amplified KRAS, with selectivity over NRAS and HRAS (preserves T-cell activity)

- Differentiation: Degrader approach overcomes compensatory KRAS upregulation seen with inhibitors; stronger anti-proliferative effects vs. pan-RAS inhibitors

- Upcoming Data: Preclinical comparison vs. pan-RAS inhibitors at AACR Special Conference on RAS in March

Full Year 2025 Financial Summary

The significant reduction in net loss reflects:

- Lower R&D spend from program prioritization (down $63M)

- Lower G&A from operational streamlining and absence of one-time lease termination loss ($43.4M in 2024)

- Share repurchases reducing share count

Q&A Highlights

On Differentiation Bar for Each Program

Jonathan Miller (Evercore) asked what data would determine if programs are truly differentiated. Management responded:

- ARV-102 (LRRK2): Must show degradation leads to different results than inhibition for a target not yet proven to modify disease

- ARV-806 (KRAS G12D): Need to exceed ~35% response rates seen with competing inhibitors and degraders to be clearly differentiated

- ARV-393 (BCL6): At the "leading edge" of competition—will compare data as it emerges

On ARV-102 ADPD Expectations

Ted Tenthoff (Piper Sandler) asked about March ADPD data expectations. CMO Noah Berkowitz outlined key questions:

- Does the drug demonstrate continued safety in older Parkinson's patients vs. healthy volunteers?

- Is LRRK2 degradation replicated at higher baseline levels seen in PD patients?

- Do biomarker patterns (GPNMB, CD68) intensify vs. healthy volunteer findings?

On PSP Development Strategy

Management clarified their approach to Progressive Supranuclear Palsy:

- Target population: PSP-RS (Richardson syndrome), the more severe and aggressive form representing ~40% of PSP patients

- Registrational endpoint: PSP rating scale is the gold standard

- Timeline: Phase 1b in H1 2026, potentially registrational trial by late 2026 pending regulatory feedback

On Pan-KRAS vs. G12D Strategy

Blake (BTIG) asked how pan-KRAS and ARV-806 coexist. Management explained:

- Pan-KRAS addresses the ~55-60% of pancreatic cancer patients with non-G12D mutations

- G12D-specific degrader may have better combinability profile with other therapies

- Degraders can overcome resistance from KRAS amplification/overexpression—key differentiator vs. inhibitors

On Partnership Strategy

Terence Flynn (Morgan Stanley) asked about partnering plans. CEO Randy Teel noted:

- With five programs potentially in clinic by year-end (4 current + HPK1), portfolio is substantial for a small biotech

- Historical precedent: Pfizer deal for vepdegestrant (2021), Novartis deal for luxdegalutamide (2024)

- Actively keeping pharma partners apprised of pipeline progress for potential future deals

Key Risks and Concerns

- Clinical Execution: Multiple readouts in 2026 create binary risk; any clinical failure could significantly impact valuation

- Vepdegestrant Partner Search: Finding the right partner while advancing toward PDUFA adds complexity

- Cash Burn: $261M operating cash burn in FY 2025; continued need to manage runway prudently

- Competitive Landscape: KRAS G12D and other targets facing increasing competition from both inhibitors and degraders

- Regulatory Risk: First PROTAC approval carries inherent regulatory uncertainty

The Bottom Line

Arvinas' Q4 2025 results will be quickly forgotten as investors focus on what could be a transformational 2026. The June 5 vepdegestrant PDUFA decision represents a potential platform-validating moment for the entire PROTAC field. Meanwhile, clinical data from ARV-102 (March) and ARV-806 (H2) could establish Arvinas as a multi-program company rather than a one-drug story.

With $685M in cash and runway into late 2028, Arvinas has the financial flexibility to reach multiple value inflection points. The question is whether the clinical data delivers.

View the full Q4 2025 8-K Filing | Company Profile | Prior Quarter: Q3 2025